How to Calculate Your Financial Runway Before Quitting Your Job

Date: January 29 2026

Have you ever sat at your desk and thought, "I need to quit my job," but then immediately wondered, "Can I actually afford to do this?" That paralyzing moment between wanting to make a career change and knowing whether it's financially viable is something I've experienced firsthand. The question that keeps most people stuck isn't about whether they want to leave, it's "How long will my savings last?" I built QuitRunway specifically to answer this question because too many talented people make career decisions based on gut feeling rather than actual numbers. Whether you're planning a sabbatical, considering freelance work, preparing for a potential layoff, or launching a business, understanding your financial runway is the first step toward making a confident career transition.

Understanding Financial Runway

Your financial runway is simply the number of months your savings will sustain you based on your current expenses. It's a concept borrowed from the startup world, where companies calculate how long they can operate before running out of cash. The basic formula is straightforward: Savings ÷ Monthly Burn Rate = Runway in Months. Your monthly burn rate is the difference between your income and expenses essentially, how much money you're spending each month.

For career transitions, this calculation becomes crucial. If you have $30,000 in savings and your monthly expenses are $3,000 with no income, you have a 10-month runway. But here's where most people make mistakes: they forget to account for severance packages that extend their runway, or they don't consider how their expenses might change when they quit their job. Maybe you'll save on commuting costs and work lunches, but you'll need to budget for health insurance if you lose employer coverage. Understanding your true financial runway means accounting for all these variables, not just doing simple division.

The reality is that financial runway matters whether you're transitioning to a new career, taking time off for parental leave, going freelance, starting a business, or planning a sabbatical to recharge. In each scenario, you need to know your numbers before making the leap.

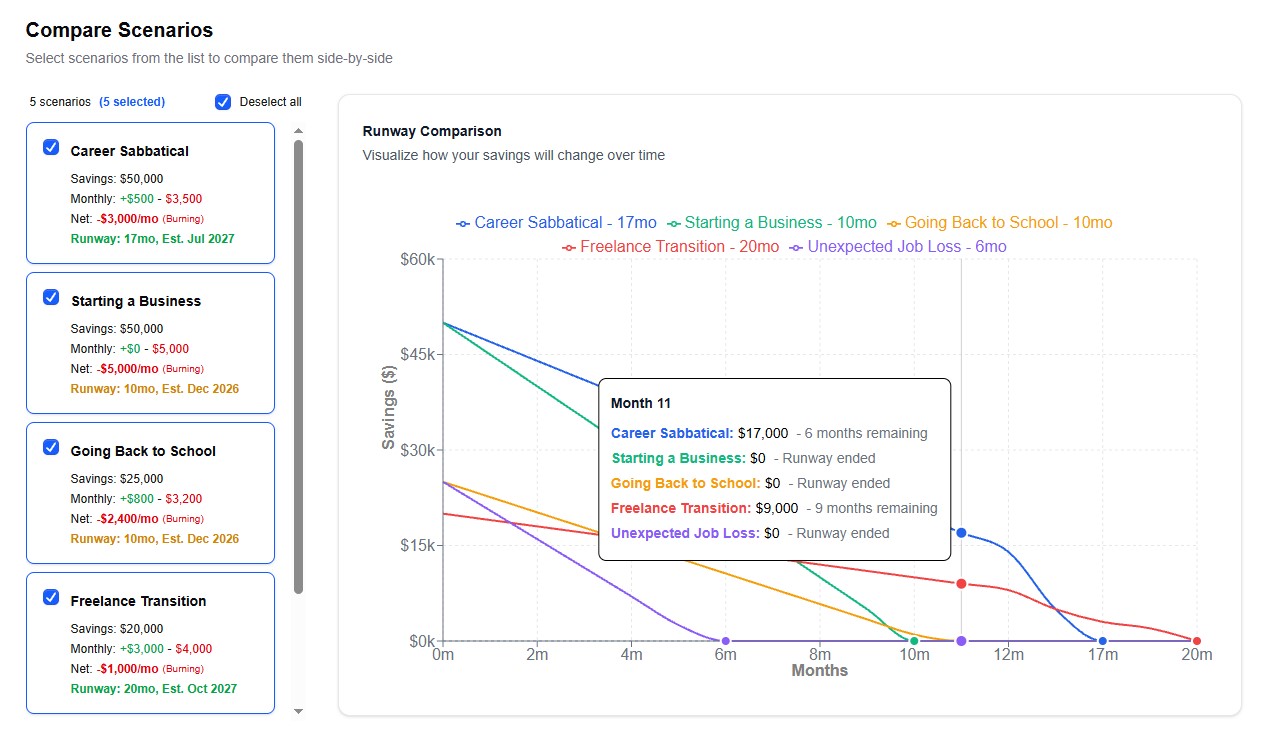

The Scenario Problem

Here's the challenge: one calculation isn't enough. When I was planning my own career transitions, I realized I wasn't choosing between "quit" or "stay" I was comparing multiple possible paths. Should I take a severance package and search for a new job? Should I go freelance and keep some income flowing? Should I start that side project full-time? Each option has different financial implications.

This is where scenario comparison becomes essential. You might have one scenario where you quit your job with a three-month severance package, giving you $45,000 in total runway. Another scenario might involve freelancing part-time while you build a business, reducing your expenses but maintaining some income. A third scenario could be staying at your current job while saving aggressively for six more months. Without comparing these scenarios side-by-side, you're making decisions in the dark.

When I built QuitRunway, I focused heavily on this scenario comparison feature because it's the difference between guessing and planning. You can create different scenarios (the free version allows up to three), adjust the variables, and see exactly how each path affects your runway. The visual charts make it immediately clear which option gives you the most breathing room.

How I Approach Runway Planning

I built QuitRunway as a side project because I saw a gap in available tools for people planning career transitions. Most financial calculators are either too simple (just basic division) or too complex (requiring you to input hundreds of data points). I wanted something in between powerful enough to model real scenarios, but simple enough to use in minutes.

Here's how it works: you enter your current savings, monthly income, and monthly expenses. If you're expecting severance, you add that too. Then you create scenarios. Maybe Scenario 1 is "Quit and Job Search" with zero income for six months. Scenario 2 might be "Freelance Transition" with reduced but consistent income. Scenario 3 could be "Start a Business" with startup costs factored in. Once you've set up your scenarios, QuitRunway generates charts showing your runway timeline for each path, making it easy to compare them at a glance.

What I find most valuable are the what-if sliders. You can test assumptions without recreating entire scenarios. What if my expenses are 20% higher than I think? What if I land freelance clients faster than expected? What if I need to pay for COBRA health insurance? These questions are critical, and being able to answer them with real numbers removes so much anxiety from the decision-making process.

You can try the free calculator right now, no signup required and model your own scenarios in minutes.

QuitRunway is designed for anyone facing a career transition: people planning to quit their job, freelancers going independent, entrepreneurs launching businesses, parents preparing for parental leave, or anyone wanting to take a sabbatical. It's privacy-first (I don't sell your data), offers transparent pricing (free for up to 3 scenarios, $6.99/month or $59/year for unlimited scenarios), and focuses on giving you the information you need without overwhelming you.

Of course, it's important to note that QuitRunway is a calculator, not financial advice. For major life decisions, I always recommend consulting with a professional financial advisor who can provide personalized guidance based on your complete financial situation.

Ready to see your numbers? Use the free QuitRunway calculator to enter your savings, income, and expenses and compare up to three scenarios side-by-side. No signup required, and you'll have your runway projections in minutes.

Practical Tips for Planning Your Runway

Beyond just running the numbers, here are some practical lessons I've learned about financial runway planning:

Build a Safety Buffer. Don't cut your runway too close. If your calculations say you have 12 months of runway, plan as if you only have 9 months. Unexpected expenses always come up, and you don't want to be forced into a bad decision because you ran out of money two months earlier than expected.

Account for Healthcare and Benefits. Losing employer-sponsored health insurance can be one of the biggest financial shocks when you quit your job. Research COBRA costs, marketplace plans, or spouse's coverage options before you make the leap. The same goes for other benefits like 401(k) matching, stock options, or commuter benefits.

Test Different Expense Scenarios. You might think you can live frugally, but actually test it. Try living on your reduced budget for a month or two while still employed. Can you really cut your spending by 30%? Or will you need more flexibility? Use a runway calculator to model both your optimistic and realistic expense projections.

Don't Forget Severance and Unemployment. If you're being laid off or negotiating an exit, severance packages can significantly extend your runway. Similarly, unemployment benefits (if you qualify) can provide a crucial cushion. Factor these into your calculations, but verify the actual amounts and timing before relying on them.

Plan for Worst-Case Scenarios. What if your job search takes twice as long as expected? What if your freelance clients dry up? What if your business takes longer to become profitable? Run the numbers on these pessimistic scenarios too. If you can survive your worst-case scenario, you'll feel much more confident making the career change.

Key Takeaways

As you consider your own career transition, here are the essential lessons for calculating and planning your financial runway:

-

Know Your Numbers: Before making any major career decision, calculate your actual financial runway. Don't guess or use rough estimates sit down and do the math with real figures from your bank statements and budget.

-

Compare Scenarios: Don't rely on a single calculation. Model different paths (quit vs. stay, freelance vs. full-time, etc.) and compare them side-by-side. The right choice becomes much clearer when you can see the numbers for each option.

-

Test Your Assumptions: Use what-if analysis to stress-test your plan. Adjust your expenses up and down, change your income projections, and see how sensitive your runway is to these variables. This preparation will help you avoid nasty surprises.

-

Build a Buffer: Give yourself more runway than you think you need. A safety margin of 20-30% can make the difference between a successful transition and a stressful scramble back to employment.

-

Seek Professional Advice: While tools like runway calculators are helpful for planning and comparison, they're not a substitute for personalized financial advice. For major career changes, consider consulting with a financial advisor who can review your complete financial picture and help you make the best decision for your situation.

Final Thoughts

Planning a career transition doesn't have to feel like a leap into the unknown. By calculating your financial runway, comparing different scenarios, and testing your assumptions, you can make confident decisions based on real data instead of fear or guesswork. Ready to get started? Try the free calculator to run your numbers and compare different scenarios, or build your own spreadsheet the key is to actually calculate your runway before you make the leap. Your future self will thank you for taking the time to plan properly.